Every week, we tap into real conversations had by our pro investor community, the Curation Collective, recapping their high conviction themes, macro views and market sentiment, so that you can make more informed investment decisions.

Most Discussed...

All Eyes on the Prize

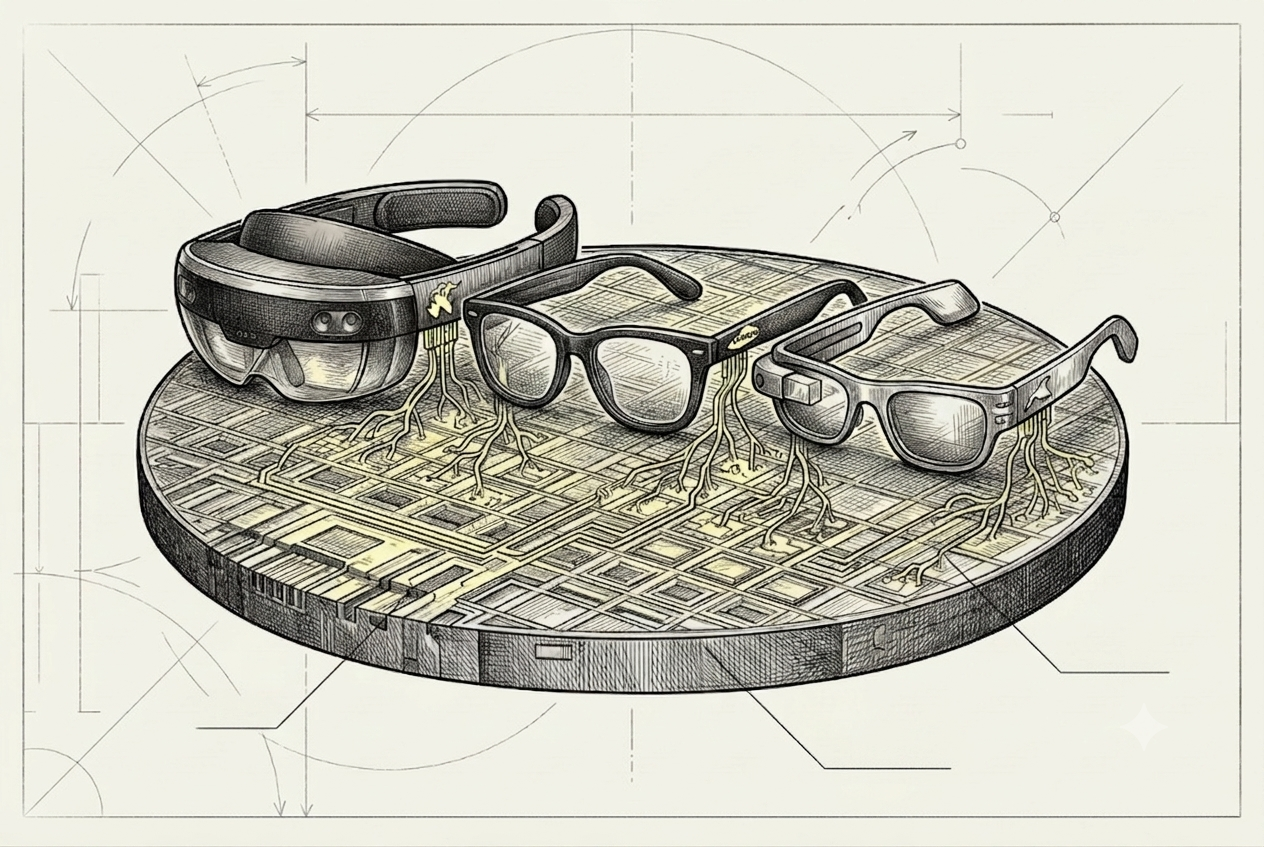

Last week, Snap launched standalone AR glasses. They work without a separate device to power them, but they are bulky, hard to miss on the face, and priced too high for the young users the platform relies on, all while the company is still lossmaking. The bigger issue is what the glasses are for: a photos-and-chat app people dip into is not something they need on all day, and the brand is not one most people want to wear on their face.

The winners are likely to be the ones who bring either an ecosystem or a trusted brand. Meta proved it with Ray-Ban. Samsung and Google are following, branded frames with an assistant wired straight into Search, Maps and Gmail. They are folding glasses into ecosystems people already live inside. Early adopters wearing them daily point to the same three benefits: live translation, always-on assistance, and a camera that holds its own against an action cam.

If smart glasses become another ecosystem war, traditional eyewear faces a harder question than it looks. The corrective-lens moat that has underpinned the industry for decades is being squeezed from both sides: Meta, Google, Samsung and eventually Apple pulling the frame into a platform fight, and longer-term scientific advances, from presbyopia drops and better refractive surgery to implantable lenses and gene therapy, chipping away at why people need glasses at all. None of that is tomorrow's problem, but it changes the multiple the market should pay for the category.

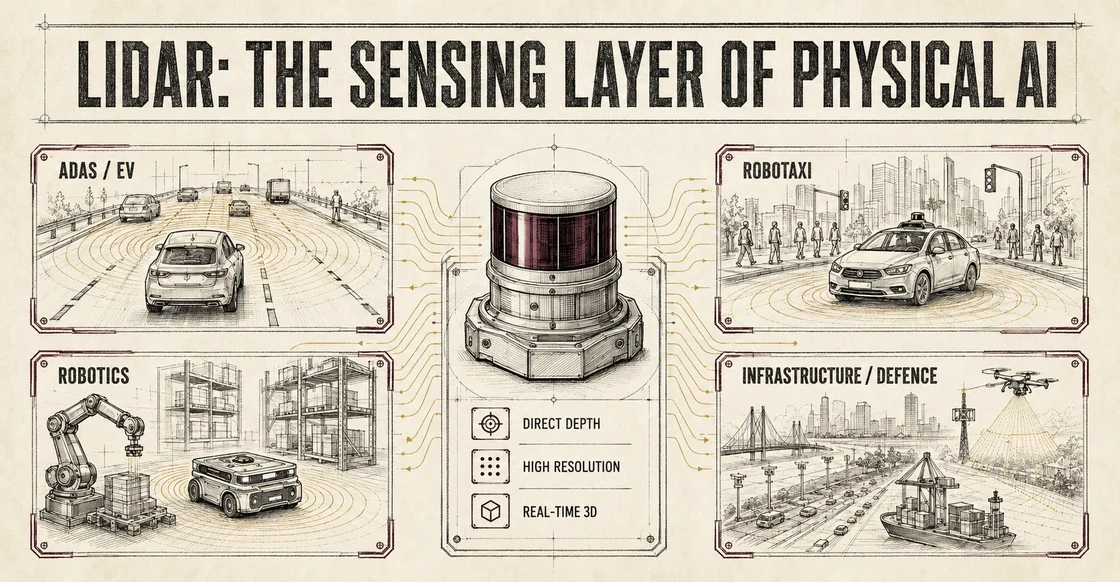

The cleaner risk/reward sits less with the brands trying to defend the frame, and more with the enabling hardware beneath the whole category. Every pair of smart glasses needs three layers of semiconductor technology to work: low-power wafers that let an AI assistant run all day without killing the battery, radio wafers that handle connectivity as glasses cut the tether to the phone, and optical wafers that shrink displays and lenses small enough to fit inside a normal frame. Whichever brand wins, those wafer and chip suppliers still get paid.

That is the pattern across the wearable-AI build-out more broadly. The silicon layer is diversifying fast, moving from smartphones into spatial computing headsets, personal AI devices, and now glasses, while the semiconductor companies behind it are making strategic moves into eyewear partnerships and acquisitions to own more of the value chain. The compute that powers on-device inference is becoming as important to the frame as the lens. The picks, not the prospectors, remain the preferred plays.

The Great Wait of China

China's May retail data released last week showed exactly why the consumer-internet thesis remains difficult to own. May retail sales fell 0.6% year on year, the first contraction since December 2022 and a clear miss against expectations of a flat print. The composition was worse than the headline: car sales down 16%, home appliances down nearly 16%, furniture and building materials both deep in the red. This is not a consumer slowing at the margin; it is one that has pulled back sharply. Government liquidity is flowing into high-tech and industrial capacity rather than into the household.

The obvious catalyst is stimulus. The same weak data weighing on the consumer complex is now increasing pressure on Beijing to act, with economists expecting policy fine-tuning in July after second-quarter GDP is released. But a short-term market reaction is not a lasting fix. The trade-in subsidies earlier this year helped for a few months, then faded once the money ran out. Only sustained household support can bring demand back properly. The setup is binary and externally timed, and until it arrives the macro keeps the lid on.

What Drove The Collective Ideas This Week

WoW: 2.3%

The Conviction basket gained 2.3% last week in a holiday-shortened session shaped by geopolitics, central-bank signalling and real commercial traction. A US-Iran peace deal sent oil sharply lower and took heat out of defence-linked positions, while the Federal Reserve's first meeting under its new chair held rates unchanged but leaned hawkish, projecting slower growth, higher inflation and a possible rate hike later in 2026. The upside came from the physical-AI and wearable-silicon corners of the book, where new commercial partnerships, manufacturing scale-ups and product launches showed the diversification thesis translating into real revenue rather than just narrative. The downside was limited to defence hardware giving back gains as the geopolitical risk premium eased on the peace headline. The thesis across the book remains intact; last week confirmed that commercial execution, not macro sentiment, is doing the work.

Find out more about Collective ideas on CurationAI.

Best Content Shared This Week

🎧 Whale Rock's AI Stack Playbook

Why Listen? Alex Sacerdote explains how one of the best-performing tech investors is underwriting the AI cycle, using Anthropic as the starting point to map the entire stack from chips and models to applications. The discussion is a useful framework for identifying where S-curves, durable moats and underappreciated earnings power are forming as AI moves from narrative to operating leverage. Listen here.

🎧 Why Nuclear's First Boom Worked and Why the Next One Is Harder

Why Listen? This unpacks one of the biggest misconceptions in energy investing: that nuclear power was once inherently cheap. The discussion explains how GE and Westinghouse effectively subsidised the industry's first expansion, why that model disappeared, and what it means for today's nuclear renaissance. A useful framework for understanding where the real bottlenecks sit in nuclear today, financing, construction risk and who is willing to absorb them. Listen here.

Stock Of The Week

The Silicon Beneath the Silicon

Soitec is not a chip designer. It sits one layer further down the semiconductor stack, producing the engineered wafers that make modern chips faster, more efficient and more capable. Its technologies are embedded across smartphones, automotive electronics, power semiconductors and the growing edge AI ecosystem, where performance and energy efficiency are becoming increasingly important.

The investment case rests on a simple idea: every new generation of AI, connectivity and electrification requires more sophisticated semiconductor materials. As chips become smaller and more powerful, the substrate beneath them matters more. Soitec's specialised platforms help improve bandwidth, power consumption and thermal performance, giving it a critical role in markets ranging from RF communications to silicon carbide power devices.

If AI is moving from the cloud into vehicles, industrial systems, and edge devices, Soitec offers exposure to the infrastructure layer that enables this transition, without having to pick a winner among chipmakers.

New or Updated Showcases

CMC Markets

CMC Markets is evolving from a traditional CFD and spread-betting platform into a broader financial infrastructure business spanning retail investing, institutional technology and platform services. Alongside its established trading franchise, the company is building recurring revenue streams through white-label partnerships, stockbroking and technology solutions, positioning it to benefit from growing demand for digital financial infrastructure while still generating strong cash flows from its core business. Read more.

.png)